Under the Federal Constitution, the Swiss National Bank (SNB) has two objectives in its mandate: monetary policy must ensure that the currency retains its value and the economy must be able to develop appropriately. As a fully independent entity, the SNB is tasked with pursuing a monetary policy serving the general interests of Switzerland. More specifically, it must ensure price stability while taking into account economic developments and determining interest rate trends through its monetary policy. It influences the money supply as well as the money stock and is the only bank that can create and destroy money. To do this, the SNB has several instruments, the main ones being the purchase of foreign currencies and granting loans to commercial banks.

The central bank grants loans to commercial banks, which pass these funds on to the public. These loans affect the money in circulation, and credit prices influence the demand for financing, particularly for housing.

Three Key Parameters Determining the Structure of Interest Rates

- the economic situation;

- the “confidence climate,” referring to investors’ and the public’s trust in the markets;

- the central bank’s stance.

Rate Increases Influence:

- the cost of a real estate project – increase in real estate prices

- slows down construction activity, stabilizes supply, and raises prices in the medium term.

- real estate valuation – decrease in prices (little short-term impact)

- methodology for discounting cash flows is based on a risk-free rate smoothed over 50 years. This avoids excessive volatility in valuations, but a rate increase reduces real estate value. However, the rise must be significant to affect the smoothing effect over a short period.

- mortgage lending – decrease in prices

- tightening of credit granting conditions, thus reducing demand.

- cost of mortgage credit – decrease in prices and income because operating expenses (mortgage charges) increase

- mortgage charges rise, leading to a drop in demand.

- rent increases – increase in income and prices

- pass-through of interest rate hikes and inflation (CPI) to rents. Commercial rents are indexed, so the increase is immediate. Rate hikes are generally accompanied by inflation and thus a likely rise in income, i.e., rents. This mechanism somewhat protects real estate in a gradual increase context, as the pass-through of inflation to residential rents takes time.

- investment returns – decrease in prices

- the attractiveness of other asset classes influences real estate prices (demand). Real estate’s safe-haven status attracts investors due to the stability of rental income but may lose some appeal if rates rise.

According to experts, the 1990 scenario of a rapid rate increase is unlikely to recur. A very gradual rate hike is forecast but not within the next five years.

Other Variables Influencing Real Estate

- construction investments (influence supply);

- GDP growth (influences supply and demand);

- interest rates (influence supply and demand);

- household income (influences demand);

- demographic changes (influence demand);

- exchange rates (influence demand).

Supply decreases or demand increases: prices rise

Supply increases or demand decreases: prices fall

When the Construction Sector Does Well, Everything Does Well?

Everyone knows this famous saying. The health of an economy is measured by the strength of the construction sector. What are the direct effects of the economic situation on real estate?

To demonstrate the complexity of these variable combinations, the independent expert Wüest & Partners developed a model that calculates various factors affecting housing prices.

According to these calculations: “when the population increases by 1%, prices rise by 3% (condominiums) and 0.6% (single-family homes). And if inflation rises by 1%, the value of condominiums and single-family homes will increase by 3.9% and 2.4%, respectively.” But these are mathematical assumptions, notes Hervé Froidevaux, partner at Wüest & Partner in Geneva, in his 2015 interview with the newspaper Le Temps. “If inflation rises, growth can also be expected to change. So it is about combining these variables.”

AND What Does Imvesters Do to Protect Itself?

Imvesters protects expected returns by provisioning conservative operating expenses to cover unforeseen costs, such as an increase in operating expenses. Additionally, real estate crowdfunding investments are limited to a first-ranking mortgage loan (maximum 66%), which helps protect owners in case of property devaluation and the impact of rising mortgage charges.

Finally, mortgage rates are fixed to avoid risk over the investment period. As noted above, rising rates also tend to increase rents, especially commercial rents, which are indexed. A thorough analysis is conducted on each file and the macroeconomic situation. Rental potential and all the factors mentioned are well known to the experts on Imvesters’ property selection team.

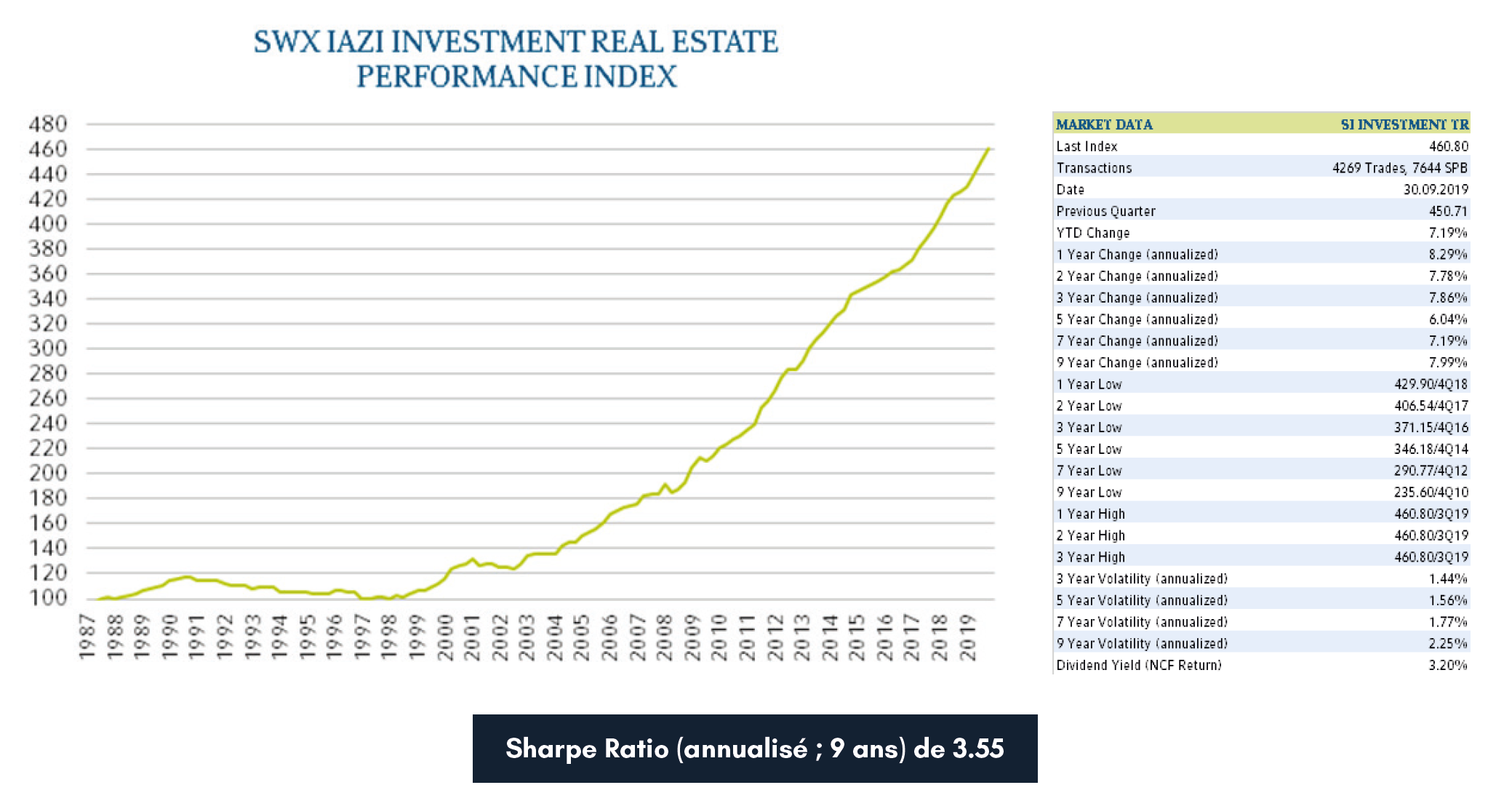

Real Estate Performance (Total Return) from 1987 to 2019

Total return: net yield and real estate prices

Introduced in 1966 by American economist William Forsyth Sharpe, the Sharpe ratio measures an asset’s profitability relative to the risk of its underlying compared to a risk-free rate, such as a Swiss Confederation bond.

Indeed, according to this economist, average returns alone are insufficient to measure an asset’s true performance. The Sharpe ratio’s goal is to enable an investor to analyze the level of excess return obtained relative to the additional risk taken to generate that return.

Generally, a Sharpe ratio above 1 is considered acceptable by investors. A ratio above 2 is regarded as very good, and a ratio of 3 or more is considered excellent.

Key Takeaways

Interest rates are one of several factors influencing changes in property prices or income. Risk is controlled and measured when the investment is managed by professionals who are close to their market and economic indicators. Rising rates do not necessarily negatively impact real estate prices. Rather, it is the magnitude of the rate increase that can have a negative effect on prices.

Conservative provisions, fixed mortgage rates, and optimal property management help navigate macroeconomically sensitive and technical periods. The IAZI Performance Index graph demonstrates that the total return of the real estate asset class has allowed investors to weather various crises while achieving an attractive return with lower risk (see Sharpe ratio).

However, it is important to be accompanied by professionals when embarking on real estate investment.