Is it possible to make your LPP assets work and take control of them?

We all hear about the LPP, but who can simply explain what it really is? Some will define it as the "2nd pillar", which is indeed quite accurate.

And if you’re asked "what is it for?", many will answer, "buying a primary residence". Yes, that’s not bad, but it’s not the only purpose!

The abbreviation LPP primarily stands for the "Federal Law on Occupational Old Age, Survivors and Disability Pension Provision" and defines the minimum benefits you receive from your occupational pension in one of the cases mentioned in the definition.

You should understand that the goal of your LPP is to supplement the benefits paid by the AHV (Old Age and Survivors Insurance) to guarantee, upon retirement, an income equivalent to 60% of your last salary. Its objective also covers your needs in case of disability and those of your loved ones in case of death. Simple as can be, isn’t it?

WHAT IF I STOP WORKING?

"If I stop working, what happens to my LPP?" Your LPP still exists, but it will transform into a free passage account.

Hmm, pardon, what’s that?

It’s simply the term used to designate the account where the pension capital you have accumulated is deposited. When you are no longer employed, a free passage account is created. It is reserved for occupational pension funds—that is, your 2nd pillar. And unlike a regular savings account, a preferential interest rate is applied to this free passage account.

For example, you might be moving to live your American dream or simply traveling abroad, pursuing further education, or you might be unemployed while searching for your next dream job. In any case, your future employer is not yet known; you are starting an entrepreneurial venture, in short, there is a temporary and/or provisional interruption in your professional life.

Opening your free passage account thus guarantees the maintenance of your occupational pension until you resume gainful employment.

But what happens if your assets in this account are not invested within 6 months following the end of your employment? You might not have known, but your benefits are automatically transferred to the supplementary institution (the organization managing forgotten or unused assets) with an interest rate of 0.01%... not great, as they say!

The numbers speak even louder: The legal minimum interest rate for LPP assets is 1% (0.125% for the supra-mandatory scheme), while the average interest rate for free passage accounts is 0.022%.

As you can see, the return on LPP and free passage assets without active management is negligible, even close to zero.

"OK, I’ve read and understood what the LPP and free passage are. I’m clearly depressed knowing I can’t touch this money before retirement and, worse, I can’t do anything with it right now. Great article... so what do I do now?"

WHAT DO I DO WITH MY LPP?

Well, you get informed and look at the solutions available to you, simply with the aim of being prudent—you’ll notice the subtlety of the term chosen.

The proposed solution: real estate... "Yeah, as usual," you might say.

Some companies like Imvesters offer properties for co-ownership purchase to individuals who want to invest in real estate to earn a return on their invested sum. You don’t live there, you don’t manage tenants or property management. It’s purely about a return of around 6% annually. In practice, you invest CHF 20,000 in a building in Neuchâtel, for example, and voilà, CHF 1,200 per year credited to your bank account.

"But then, what’s the connection with the LPP? Aren’t we talking about different things?"

There might be a connection—imagine managing your free passage account like you manage your bank account.

Because, let’s be honest, apart from reading that annual statement showing your assets, we’re not sure you do much else with it... right?

Thanks to Imvesters, you can convert your LPP account and take control of your assets by investing up to 30% in real estate.

Imvesters now partners with major banking and LPP insurance institutions to allow everyone to manage their pension and add a secure added value.

CASE STUDY: MATHIAS AND PAUL

Let’s understand the mechanism through the situations of Paul and Mathias.

Mathias, 47, is an employee and human resources director at a textile company for 22 years with a very decent salary. He is married, rents an apartment in Nyon, has no intention of buying a primary residence, and wants to keep this money for his old age.

Paul, 36, is self-employed. He is single and also rents an apartment in Valais. No longer employed by an employer, he receives a letter from his former pension fund proposing to transfer his assets to another account.

Paul researches his LPP during his work interruption and hears about Imvesters’ solution to invest in real estate. He finds it interesting and tries it out. Mathias, on the other hand, does not want to get involved and leaves his LPP with his employer’s pension fund.

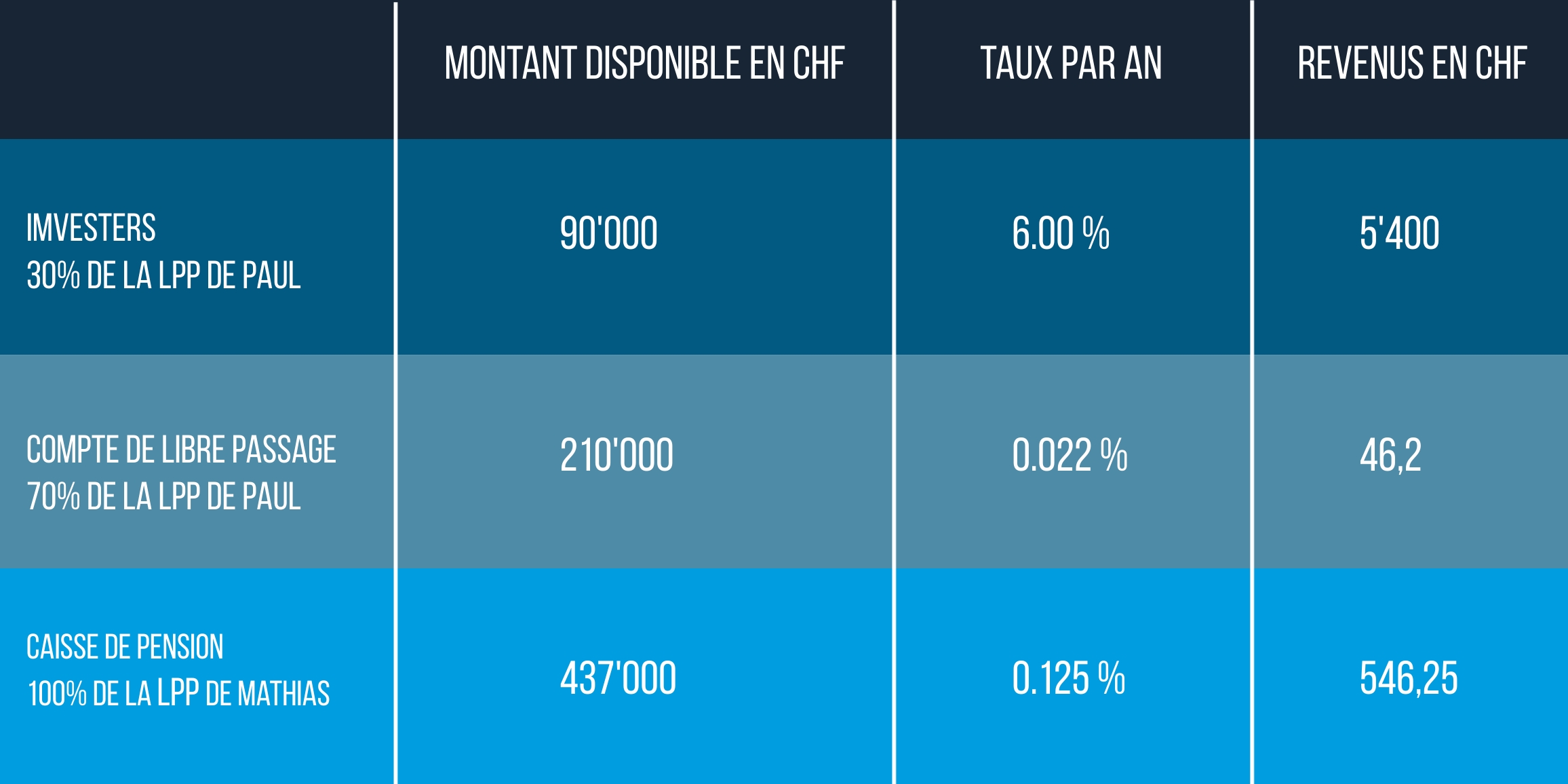

Paul then decides to invest the maximum proposed percentage, i.e., 30% of his CHF 300,000 with the pension fund partner of Imvesters.

Paul invests CHF 90,000 in a real estate portfolio offering expected returns of 6% – the remaining CHF 210,000 stays in his free passage account, which, as a reminder, yields 0.022%. Paul’s LPP thus generates CHF 5,446.20 per year on his CHF 300,000 base. Mathias’s, on the other hand, generates CHF 546.25 per year.

Incredible, isn’t it? Imagine after 10 years...

Imvesters offers secure investment solutions. Initially, the company allows investing your capital in Swiss real estate starting from CHF 20,000 and generating over 6% return on equity distributed monthly by becoming the owner of a fraction of a building registered in the land registry.

The properties are self-supporting (the income covers bank requirements for interest payments, operating costs, and building maintenance). A retiree’s file is therefore accepted for this type of investment.

For these precise reasons, it is an ideal investment to place part of your 2nd pillar capital. No constraints, low risks, whether you continue to contribute or not, your money works for you.