Annuity or Lump Sum?

To answer this crucial question about occupational pension provision for retirees calmly and without hesitation, one would need to predict the future. Indeed, the most financially advantageous choice depends on the age one will reach and the amount of annuities paid during those years. If the estimated amount is higher than the available capital, it is better to choose the annuity; otherwise, the opposite.

This difficult choice contrasts security on one side and freedom on the other.

A new solution now exists that disrupts the "heads or tails" choice retirees had to make until today.

Context

Withdraw your 2nd pillar capital and manage your income by investing this money, or receive a fixed lifelong annuity? This is a question all retirees must answer three years before retirement.

Annuity

One option available to retirees is the payment of a lifelong old-age annuity.

While the capital amount paid is known, the amount of the annuity depends on the age the beneficiary will reach.

Conversion Rate

The conversion rate refers to the percentage of retirees’ old-age capital paid annually as an annuity by pension funds.

Although the legal conversion rate is 6.8%, many pension funds apply much lower rates. For example, why do some funds apply a rate below 4.5%?

Because the legal conversion rate applies only to the mandatory parts of the retirement provision. Pension funds can freely set the conversion rate for the extra-mandatory portion.

The principle: the lower the conversion rate, the older the insured must be for the annuity payment to be more advantageous than the capital.

Many retirees seek peace of mind through a monthly annuity without exposure to investment risks.

However, the annuity offers no flexibility, as one must accept a fixed income. It is paid only to the insured until death. Any remaining balance of the pension assets after annuity withdrawal reverts to the pension fund. Moreover, annuities do not increase, even in "good years," nor do they adjust for inflation.

Withdrawing the capital allows investment according to individual needs.

Lump Sum

The Occupational Pensions Act (LPP) stipulates that at least one quarter of the accumulated old-age assets can be paid out as a lump sum upon retirement. Pension funds may, however, provide for full capital payment.

If larger expenses are planned, such as real estate purchase, travel, extraordinary expenses, or family donations, the lump sum option allows tailoring the consumption of this retirement savings to one’s needs. One can use part immediately and invest the rest long-term to generate returns.

However, given the current market, it is difficult to achieve attractive returns without taking significant risks.

Real Estate Crowdfunding

It is now possible to invest your capital in Swiss real estate starting from CHF 20,000 and generate over 6% equity returns distributed monthly by becoming the owner of a fraction of a building registered in the land registry.

The Moulin de Cugy offers an expected and secure return (with provisions for expenses) of 7.29%. This yield is higher (and risk lower) than the conversion rates applied by pension funds.

The properties are self-sustaining (income covers bank requirements for interest payments, operating costs, and maintenance). Therefore, a retiree’s application is accepted for this type of investment.

This investment allows you to:

- preserve your capital

- generate returns over 6% per year

- receive a monthly annuity

- pass on your investment to your heirs

For these precise reasons, it is an ideal investment to place your 2nd pillar capital. Real estate crowdfunding is a genuine solution to invest your retirement capital and thus provide the necessary monthly annuities for a peaceful retirement.

Transmission and Inheritance

Upon the annuitant’s death, the spouse receives a survivor’s pension amounting to 60% of the deceased’s annuity.

With the lump sum option, 100% of the remaining assets are inherited by relatives.

Real estate crowdfunding allows the transmission and inheritance of a profitable real estate investment (see chart below). It also represents the transmission of Swiss wealth.

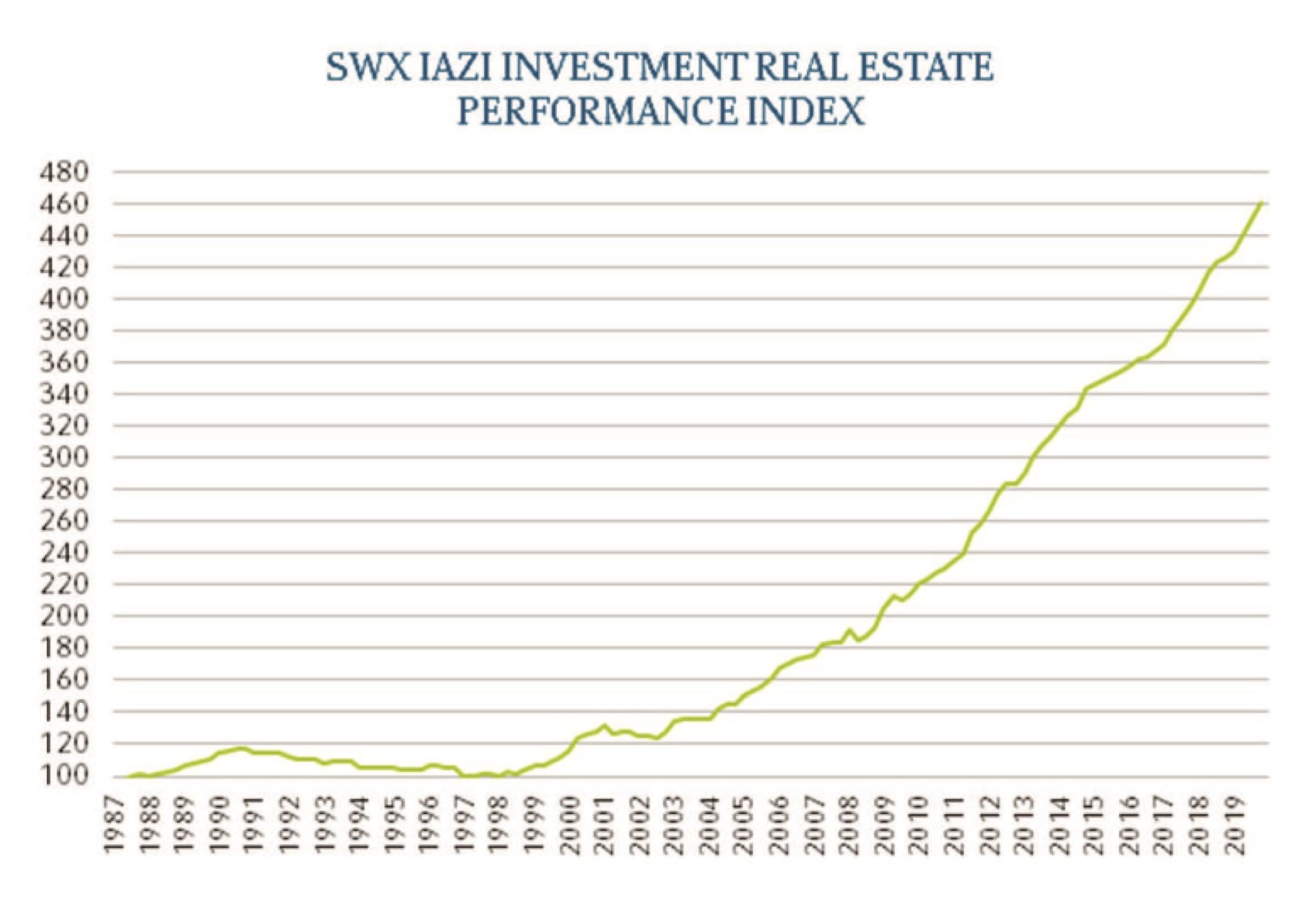

IAZI/CIFI total return (Swiss real estate prices and income)

IAZI/CIFI total return (Swiss real estate prices and income)

Key Takeaways

Neither annuity nor lump sum seemed clearly the solution; it depends on life expectancy, the conversion rate (6.8%, but subject to reduction), and the returns generated by invested capital. Current markets offer neither the security nor the returns needed for a peaceful retirement.

Real estate crowdfunding offers a new investment solution with the following characteristics: security, returns, monthly annuities, and freedom. Synonymous with peace of mind.